Hello! I’m Jay, and I’m thrilled to have you back on the blog. Today, we are talking about the dark side of retirement planning—the traps that can quietly drain your bank account if you aren’t paying attention.

Introduction

Understanding common Social Security mistakes is the only way to ensure the government check you’ve earned actually stays in your pocket. I’ve spent the last few years analyzing my own retirement trajectory, and I was shocked to find how one wrong click on a form could cost me six figures over my lifetime. In this guide, I’ll share the 5 critical errors I almost made so you can avoid the same fate in 2026.

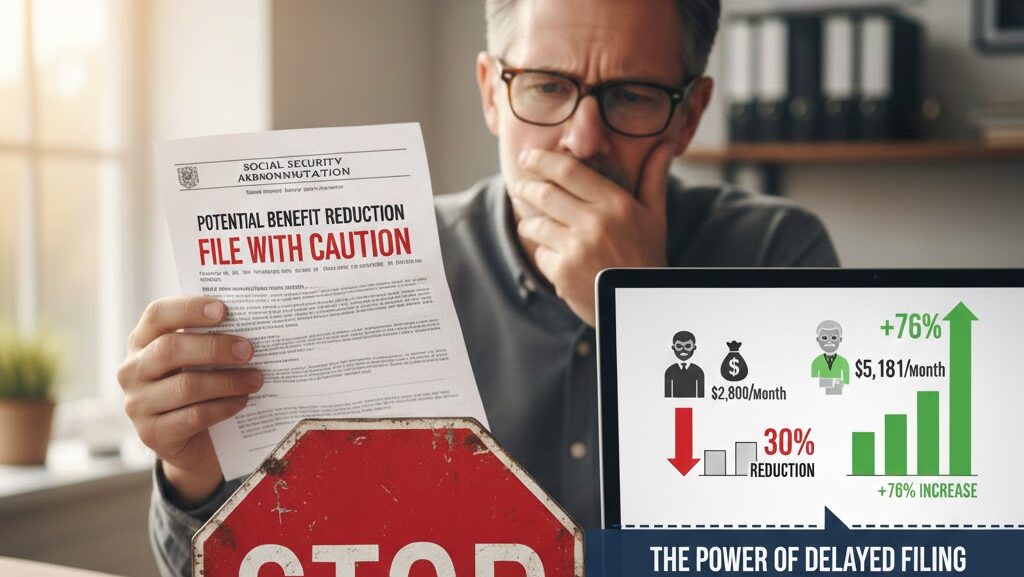

Mistake #1: Filing Too Early Without a “Longevity Plan”

The biggest of all Social Security mistakes is claiming benefits the moment you turn 62. When I first looked at my statement, the immediate cash was tempting, but I realized I would be permanently slashing my monthly check by 30%.

In 2026, with life expectancies increasing, filing at 62 means you are betting against yourself living a long life. I chose to wait because the math showed that “breaking even” happens much sooner than most people think.

If you don’t have a massive private pension, filing early is often a one-way ticket to a cash-strapped old age. I strongly recommend looking at your 70-year-old self’s needs before signing that paperwork.

Mistake #2: Ignoring the 2026 Earnings Test Limits

I once thought about claiming Social Security at 63 while continuing to work my consulting job. I quickly learned that this is one of the most painful Social Security mistakes for active workers.

If you are under your Full Retirement Age (FRA) and earn over the annual limit, the SSA withholds $1 for every $2 you earn over that limit. In 2026, these thresholds have adjusted, but they remain a massive trap for the uninformed.

I decided to stop working full-time before claiming, or simply wait until my FRA. Don’t let the government “tax back” the benefits you were so excited to receive.

Mistake #3: Forgetting the “Tax Torpedo”

Many people believe Social Security is tax-free income, but that is a dangerous myth. I was horrified to discover that if your “provisional income” exceeds a certain level, up to 85% of your benefits can be taxed.

This “Tax Torpedo” happens when you take large RMDs (Required Minimum Distributions) from your 401(k) alongside your Social Security. I mitigated this by shifting some of my assets into a Roth IRA.

By reducing my taxable income now, I am protecting my future Social Security checks from being eaten away by the IRS. It’s a chess game, and you need to be three moves ahead.

Quick Summary Checklist: Avoid These Red Flags

- [ ] Check your FRA: Don’t guess; know your exact Full Retirement Age.

- [ ] Calculate “Provisional Income”: Sum of Adjusted Gross Income + Tax-Exempt Interest + 50% of Social Security.

- [ ] Review Earnings Limits: If you’re under FRA and working, know the 2026 limit.

- [ ] Coordinate Spousal Filing: Ensure the higher earner waits as long as possible.

- [ ] Medicare Alignment: Remember that Medicare Part B premiums are often deducted directly from your check.

Mistake #4: Missing Out on Spousal and Survivor Benefits

I’ve met many couples who leave thousands on the table because they don’t understand how spousal benefits work. One of the most common Social Security mistakes is a lower-earning spouse claiming their own small benefit while ignoring a much larger spousal option.

In my case, my partner and I sat down with a calculator to see who should file first. We realized that by having the higher earner wait until 70, we were essentially buying a “life insurance policy” for the survivor.

The survivor will inherit the larger of the two checks, so maximizing that one check is the ultimate gift to your spouse.

Mistake #5: Failing to Audit Your Earnings Record

I recently logged into my my Social Security account and found a year—back in the early 2000s—where my income was recorded as $0. That was a mistake by my employer at the time.

Since Social Security is based on your highest 35 years of earnings, a single “$0” year can drag down your entire monthly payment. I had to dig up old tax returns to prove I worked that year.

Don’t assume the government has perfect records. Check your statement every single year to ensure every dollar you earned is being counted toward your future.

Step-by-Step Action Guide to Protect Your Retirement

- Create your “my Social Security” account: Do this today at SSA.gov. It’s the only way to see your actual data.

- Run a “What-If” Analysis: Use a professional calculator to see the difference between filing at 62, 67, and 70.

- Consult a Tax Pro: Ask them specifically about the “Tax Torpedo” and how your 401(k) withdrawals will affect your Social Security taxes.

- Set a Filing Date: Once you have the data, pick a date and stick to it, but remain flexible if your health or employment changes.

FAQ & Special Tips from Jay

Q: Can I change my mind after I file? Jay’s Tip: You have a 12-month “do-over” window. If you regret filing early, you can withdraw your application, but you must pay back every cent you received. It’s a tough pill to swallow, so try to get it right the first time!

Q: Will Social Security run out of money in 2026? Jay’s Tip: No. While the trust funds face long-term challenges, the system is funded by ongoing payroll taxes. Even in a worst-case scenario, the system could still pay out roughly 77-80% of scheduled benefits. Don’t let fear-mongering drive you to file too early.

Q: How do I handle Medicare? Jay’s Tip: If you are already receiving Social Security, you’ll be automatically enrolled in Medicare Parts A and B at 65. If not, you must sign up manually. Missing this window can result in permanent late-enrollment penalties!

Jay’s Personal Insight (My Final Thoughts)

In my experience, the biggest threat to your retirement isn’t the stock market—it’s impatience. We live in a world of instant gratification, and the urge to grab that Social Security check at 62 feels like winning a small lottery.

However, after looking at the numbers for 2026, I’ve realized that Social Security is the only inflation-protected, government-guaranteed annuity we have. Treating it like a “bonus” rather than a “foundation” is a recipe for disaster.

My personal strategy has always been to spend my taxable investments first and let my Social Security grow. It’s a psychological shift, but once you see that “maximized” number on your statement, the wait feels entirely worth it. Don’t let these 5 mistakes be the reason you struggle in your 80s.

It was a pleasure sharing these insights with you! Retirement should be a time of joy, not financial stress. If you stay informed and avoid these common pitfalls, you’re already ahead of 90% of the population.

Warmly,

Jay

If you enjoyed this post, you might also like: